Table of Contents

Introduction to Peer-to-Peer (P2P) Lending

What is P2P lending?

Hey there! Let’s talk about something called P2P lending. Simply put, it’s like you and I lending money to each other or borrowing from each other directly. We don’t need to go through a big traditional bank as the main source of the money.

Think of it as people helping people out financially. Rather than having a bank as the intermediary, there are specific websites or platforms that connect people who want to lend money with those who need to borrow. These platforms make it easier for everyone to find one another.

You might also hear P2P lending called social lending or crowd lending. It’s all about a community of people uniting to lend and borrow money more directly.

How does P2P lending work?

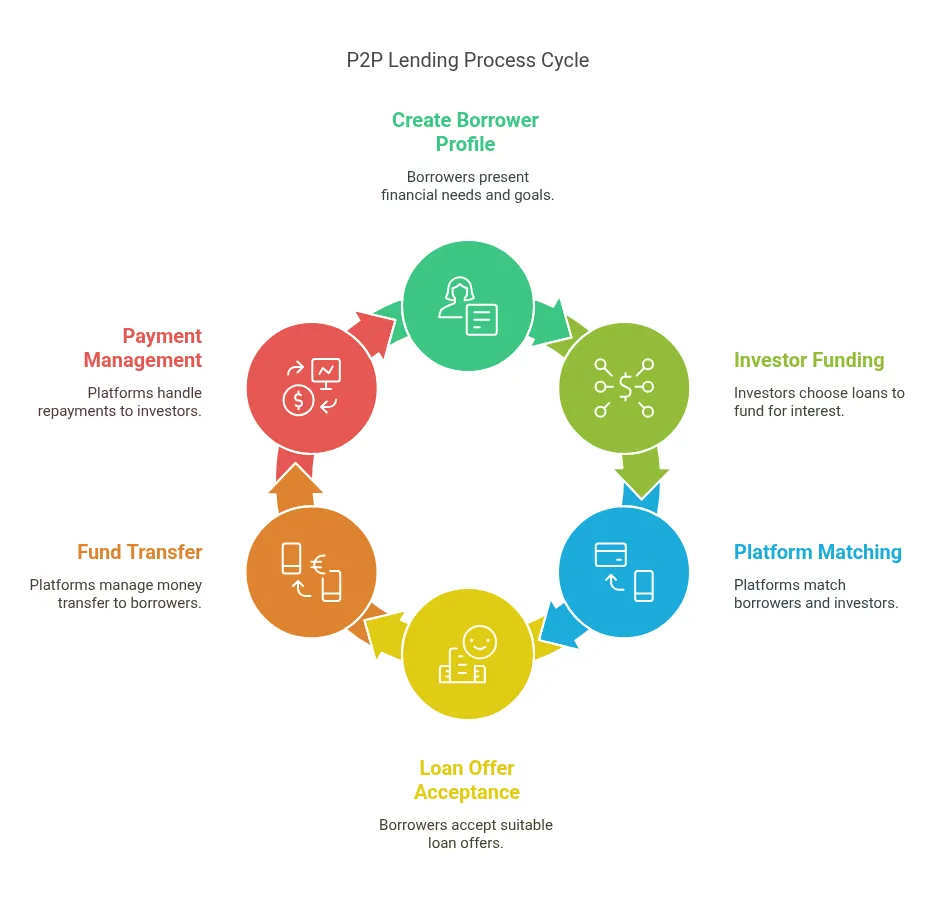

So, how does this P2P lending work? Well, it all starts with people who need money. These borrowers create profiles and tell the P2P platform what kind of loan they need. Think of it as introducing yourself and your financial goals.

On the other side, you have investors who put money into the P2P platform. These folks are looking to lend their money to earn some interest. They can often choose which loans they want to fund.

The P2P platforms are like the matchmakers here. They set the interest rates and the rules (terms) for the loans. Often, they’ll look at how trustworthy a borrower seems (their creditworthiness) to decide on these rates.

Once a borrower’s request looks good to investors, they might get loan offers. The borrower can then accept an offer that works for them. After that, the platform takes care of moving the money to the borrower and then handling the monthly payments back to the investors. It’s a straightforward way for people to lend and borrow directly.

Why consider P2P lending?

Let’s dive into why P2P lending might be a good choice.

For Borrowers:

P2P loans can be easier to get. This is true even if you don’t have a long credit history. The application processes are often simple. You might even be able to borrow larger amounts of money.

Compared to credit cards, interest rates on P2P loans might be lower. Plus, sometimes you can get the money faster than with traditional loans. So, if you need funds and want options, look at P2P lending.

For Investors:

P2P lending offers a chance for better returns. Your money could grow more than in a typical savings account. It’s also a way to spread out your investments. You can potentially help entrepreneurs and others by lending.

Investing in P2P can be a different way to make your money work for you. Just remember to understand the risks involved.

Top Peer-to-Peer Lending Platforms in 2025: A Detailed Comparison

Prosper

Prosper is a great choice if you need money fast. People also think it’s one of the best for P2P lending and even for investing. Plus, they accept folks with fair credit scores.

Prosper gets its funds in a cool way. Regular people like you and me can invest in loans through Prosper. But they also get money from bigger institutions like banks. This mix helps them to offer a variety of loans.

The interest rates you might get with Prosper range from 8.99% up to 35.99%. You can borrow anywhere from $2,000 to $50,000. You’ll have between 24 and 60 months (that’s 2 to 5 years) to pay it back.

To borrow from Prosper, you’ll generally need a credit score of 640 or higher, but they suggest at least 600. They even accept people with ‘fair’ credit. Keep in mind, there’s an origination fee between 1% and 9.99%. They’ll take this out of the loan amount before giving it to you. The good news is there’s no penalty if you pay your loan off early.

There are some nice perks with Prosper. You can apply with someone else (a co-borrower). If you borrow from them again, you might even get a better interest rate. They also let you change your payment date if needed. Plus, they have got a wide range of loan amounts.

But there are a couple of things to keep in mind. Their late fees can be high. Also, that origination fee can add to the cost of your loan.

Upstart Personal Loans

Let’s learn about Upstart Personal Loans! They are a great option for folks with a limited credit history. They also have a low credit score condition.

Upstart gets its money from institutional investors and banks. So, while it’s a P2P platform, the funding comes from bigger financial players.

The interest rates with Upstart can range from 6.70% up to 35.99%. You can borrow between $1,000 and $50,000. The loan repayment options are usually 36 or 60 months (that’s 3 or 5 years). Keep in mind they have limited repayment terms.

One of the cool things is that Upstart can work for you even with a low credit score. You might only need a low score of 300. They even consider people who do not have a credit score yet.

Be aware of the fees though. Upstart has an origination fee that can be anywhere from 0% to 12%. This amount gets taken out of your loan. Their late fees can also be high, either 5% of what you owe or $15, whichever is more. The good news is they don’t charge a fee if you pay your loan off early.

There are some good reasons to pick Upstart. They are open to people with fair credit. They also accept folks without much credit history. You will not pay a fee for paying early. Plus, they often provide fast funding, the next business day. They even look at your education and job history.

But there are some downsides. Those late fees can add up. The origination fee can also be quite high (up to 12%). They also charge $10 if you want paper copies of your loan agreement. You’ll need a Social Security number to apply. Also, you can’t apply with a co-signer or co-borrower through Upstart.

Kiva

Let’s talk about Kiva! It’s a cool platform, best for people who are starting a small business. They offer a unique way to get funding.

Kiva’s loans come from peer-to-peer crowdfunding. This means regular people lend small amounts of money. These are like microloans for entrepreneurs.

You can usually borrow between $1,000 and $15,000 through Kiva. You’ll have up to 3 years (or 36 months) to pay it back.

The amazing thing about Kiva is the interest rate: it’s 0%! That’s right, no interest. They don’t have a least credit score rule either.

To get a Kiva loan, you need to be at least 18 and a US resident. Your loan must be for a business purpose. You also can’t be in foreclosure, bankruptcy, or have liens. You’ll need some friends and family willing to lend to you first.

There are some great things about Kiva. You can borrow without any interest. It’s designed for those who struggle to get loans elsewhere. Plus, you can showcase your business to many potential lenders.

But it takes work to get a Kiva loan. You need to ask friends and family to lend to show you’re trustworthy. It can also take some time to get the full loan amount, as people need to invest. Kiva doesn’t have a Better Business Bureau (BBB) rating.

LendingClub

Let’s learn about LendingClub! It’s an interesting option, especially if you have a co-borrower or want to merge your debt.

LendingClub used to be a true P2P lender. But now, they mostly fund loans directly. So, the money comes straight from them.

The interest rates at LendingClub range from 7.90% to 35.99%. You can borrow between $1,000 and $40,000. You can pay it back over 24 or 60 months, and sometimes up to 72 months.

To borrow from LendingClub, you’ll generally need good credit. They recommend a low score of 660. There is an origination fee that can be between 0% and 8% of your loan amount.

The good news is there’s no penalty if you pay off your loan early. They give you a 15-day grace period for late payments without a fee.

Here are some good things about LendingClub:

- You can apply with someone else.

- They can send money directly to your creditors for debt consolidation.

- They offer quick decisions.

- You can even get a “Top-Up” loan to refinance.

- There are no prepayment penalties.

Keep in mind these potential drawbacks:

- They have origination fees.

- Their lowest credit score is higher than some others.

Funding Circle

Let’s explore Funding Circle! They are quite different as they focus on loans for small businesses.

They can offer funding of up to a large amount of $500,000. That can really help a growing business!

The great thing about Funding Circle is its fast approval process. You might get approved in as little as 24 hours! And you could potentially have the funds in your account in just two days.

But, they do have some specific needs. Your business needs to be operating for at least six months. Also, they usually need you to provide collateral, which is often a general lien on the business.

So, Funding Circle stands out because it specializes in business loans and is a strong source of qualified business loan leads. Plus, they offer very rapid funding for those who qualify.

Avant

Let’s dive into Avant! They aim to give you a good mix of getting your money quickly and keeping costs reasonable.

You can borrow between $2,000 and $35,000 with Avant. They offer loans in different amounts to fit your needs.

Avant has flexible repayment options. You can choose to pay back your loan in 12 to 60 months. This lets you pick a payment plan that works for you.

Keep in mind that Avant charges an administration fee. This fee can be up to 4.75% of your total loan amount.

Their interest rates are usually in the middle range. So, they are not super high or super low compared to others.

Avant is good if you need funds fast and want flexible payment choices. They also have moderate interest rates.

Happy Money (Payoff Loan)

Let’s talk about Happy Money and its Payoff Loan! This loan is specifically for tackling credit card debt.

If you have many credit card balances, this might help. You can borrow between $5,000 and $40,000.

They offer flexible repayment terms. You can choose to pay back the loan over 2 to 5 years. This helps you find a comfortable payment plan.

There is an origination fee to consider. This fee can range from 1.5% to 5.5% of the loan amount.

Happy Money’s Payoff Loan is a good option if you want to merge your credit card debt. They have flexible terms and their fees are competitive.

LightStream

LightStream is a good choice for people who have got good or excellent credit.

They offer loans for specific reasons. These include things like home improvement and debt consolidation. You can also get loans for cars, medical bills, weddings, and adoption.

One of the best things about LightStream is its competitive interest rates. They even have a “Rate Beat” program. If you find a lower rate elsewhere and meet their rules, they might beat it!

They also offer flexible repayment terms. This means you can often choose how long you want to pay back the loan. Plus, their loans are designed for a specific purpose.

But, it’s important to know that LightStream has strict credit requirements. So, you’ll likely need a strong credit history to qualify.

SoFi

Let’s explore SoFi! They are known for their friendly approach to borrowers.

One of the best things about SoFi is its competitive interest rates. This can help you save money over the life of your loan.

SoFi offers a variety of lending options, including small business loans that are designed to help entrepreneurs and business owners access the capital they need to grow. Their business financing stands out for the same reason their personal loans do, competitive rates and borrower-friendly terms.

Even better, SoFi doesn’t charge many of the common loan fees. You won’t have to worry about origination fees or late fees, which are great.

They also have a unique benefit. If you lose your job and are eligible, you might be able to pause your loan payments for a bit. This can give you peace of mind during tough times.

SoFi has policies that are designed to help borrowers. They focus on making the borrowing process easier and more affordable.

Pros and Cons of Peer-to-Peer Loans

Let’s talk about the good and not-so-good things about peer-to-peer (P2P) loans. These apply if you want to borrow money or invest in loans.

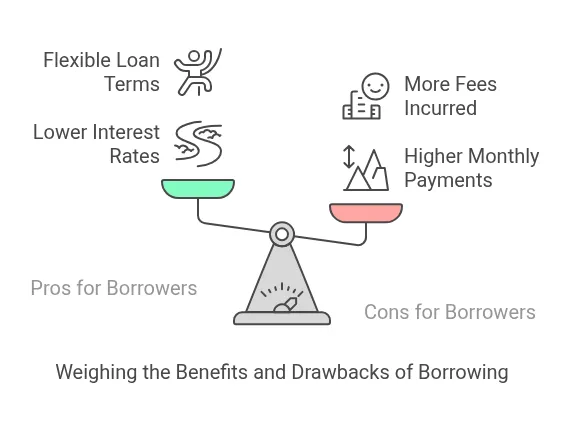

Pros for Borrowers

For borrowers, one big plus is lower interest rates compared to credit cards. You might also pay off your loan faster with shorter terms. In some cases, the application can be quicker. If your credit isn’t perfect, qualifying might be easier on some platforms. You can often find flexible loan amounts and terms.

Cons for Borrowers

Shorter repayment terms mean your monthly payments could be higher. You might also face more fees than with traditional loans. For example, there could be origination or late fees. If your credit isn’t great, the interest rates could still be high. Also, not all platforms let you apply with a co-borrower.

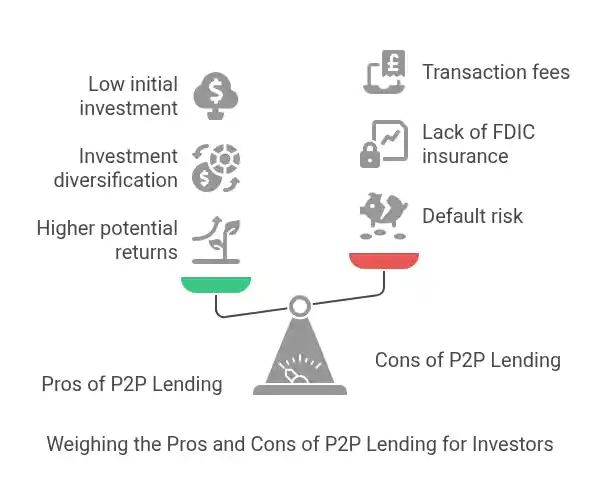

Pros for Investors

For investors, P2P lending can offer higher potential returns than savings accounts. It’s also a way to diversify your investments. Some platforms let you start with a small amount of money, like $25.

Cons for Investors

The biggest one is borrowers not paying back their loans (default). Default rates can be higher than with traditional banks. Your investment is not protected by FDIC insurance. The platform itself could face problems or even go bankrupt. Finally, the platform might charge you transaction fees.

Is Peer-to-Peer Lending Safe?

Let’s talk about how safe peer-to-peer lending is. It’s good to think about this if you want to borrow or invest.

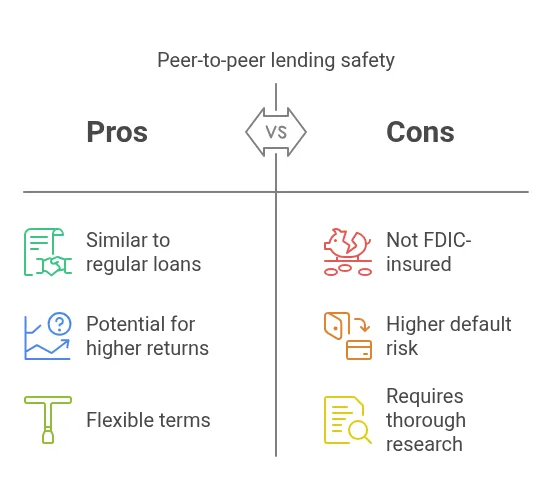

For borrowers, P2P loans are generally as safe as regular loans. Just make sure you understand all the terms and fees before you sign up.

For investors, it’s a bit different. P2P lending is riskier than keeping money in a bank. This is mainly because your money is not FDIC-insured.

Also, there is a higher chance that people who borrow might not pay back the loan. So, investors take on more risk.

Investors need to research the P2P platform carefully. Look into its reputation and how stable it is financially. This can help you make a smarter choice.

What Credit Score Do You Need for a P2P Loan?

Let’s talk again about the credit score you need for a P2P loan. Just like we discussed, it really depends on the platform you choose.

Generally, having a higher credit score is helpful. It often means you can get better interest rates and loan terms. Lenders see you as less of a risk.

But, some P2P lending sites are more open to people with lower credit scores. Some even work with people who are new to credit.

For example, Upstart is known for this. They say you can sometimes get a loan even with a credit score of 300. They even consider applicants with no credit history. Kiva also has no least credit score rule.

But, Prosper generally looks for a credit score of 640 or higher. LendingClub also tends to prefer borrowers with good credit.

So, when you’re looking for a P2P loan, make sure to check the credit score requirements for each platform. This will help you find the right fit for your situation.

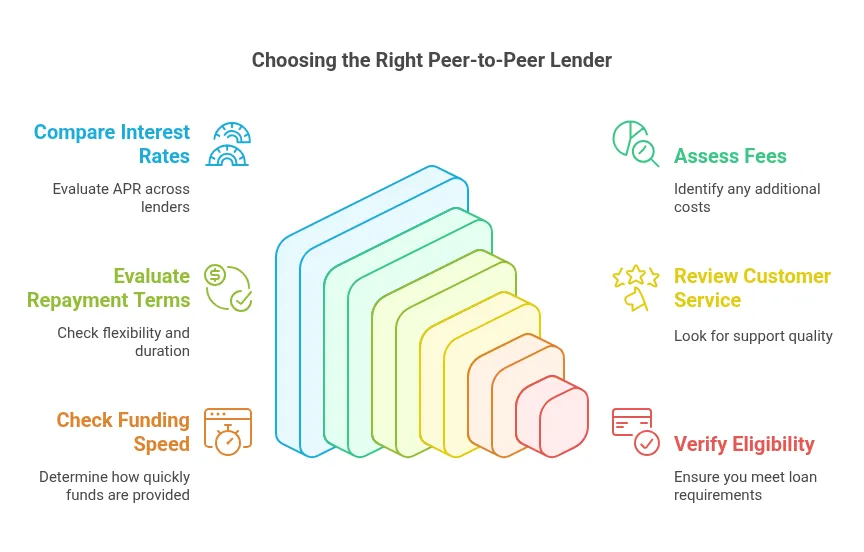

How to Choose the Right Peer-to-Peer Lender

It’s smart to think carefully about choosing the right peer-to-peer lender! There are a few important things to look at.

- First, think about interest rates. You want a lender with a good rate. Compare the APR (Annual Percentage Rate) between different lenders. A lower APR can save you money.

- Next, consider fees. Some lenders charge origination fees or late fees. See what fees each lender has. Also, check if there are prepayment penalties.

- Repayment terms matter too. How long will you have to pay back the loan? See if the lender offers a flexible schedule or a loan length that works for you.

- Think about customer service. It’s good to know the lender will help if you have questions. Read reviews from other borrowers to see what their experience was like.

- How fast you can get the money is also key. If you need funds quickly, check the lender’s funding speed. Some can get you money fast.

- You also need to check if you qualify for a loan. Look at their eligibility requirements. This includes things like your credit score and maybe your income.

- Finally, see what loan amounts each lender offers. Make sure they can lend you the amount of money you need.

Here are some steps to help you choose:

- Research and compare different P2P lenders. Look at their websites and what they offer.

- Check if you can get a pre-qualification offer. This can give you an idea of rates and terms without hurting your credit score.

- Read reviews and testimonials from other people who have used the lenders. This can give you good insights.

By looking at these things, you can find the right peer-to-peer lender for you!

How to Apply for a Peer-to-Peer Loan

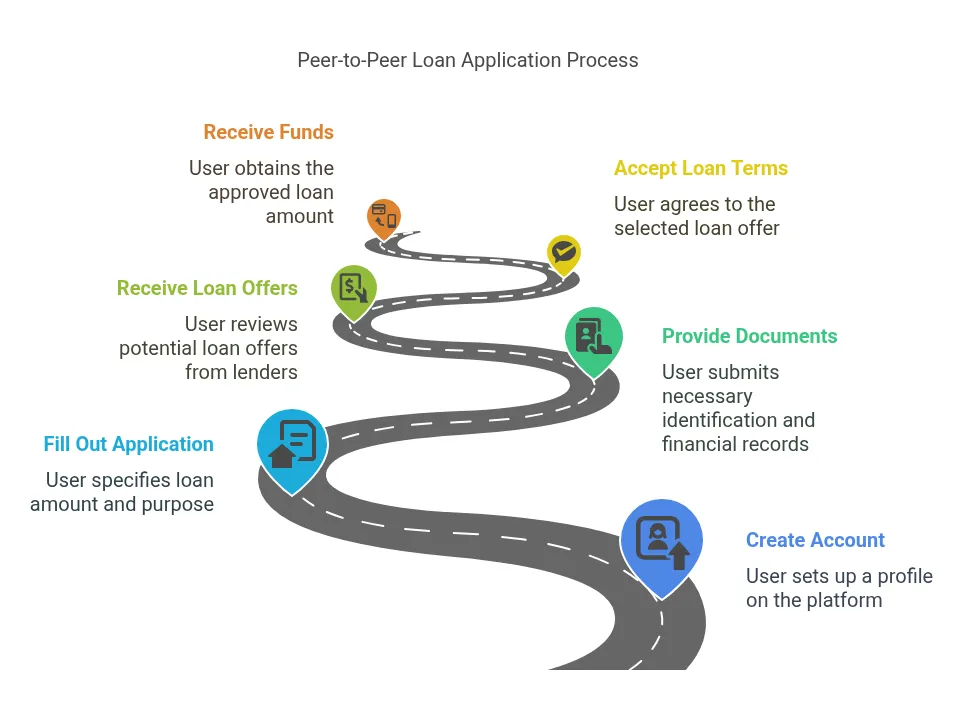

Applying for a peer-to-peer loan is like starting a new financial journey! Let’s break down the steps to help you understand.

- First, you need to create an account on the P2P lending platform you choose. You’ll share some basic personal and contact information. Think of it as saying hello!

- Next, you will fill out the loan application. Here, you’ll tell them how much money you need. You’ll also say why you need the loan and how long you want to pay it back. You’ll share some info about your financial history too.

- You’ll also need to provide some documents. This might include proof of who you are. You might need to show your financial records. Proof of where you live, your income, and your job could also be needed. Having these ready will make things easier.

- After you apply, you’ll get loan offers. It’s super important to review these carefully. Look closely at the interest rates, the repayment terms, and any fees involved.

- Once you find an offer you like, you’ll accept the loan terms. This is like saying, “Yes, this looks good to me!”.

- Then comes the good part – receiving your funds! Often, the money is sent directly to your bank account. This is usually a quick way to get the money.

- Finally, you’ll need to manage your loan repayments. Making on-time payments is key. Consider setting up auto-pay so you don’t miss a payment. Keep an eye on your progress. If you think you might have trouble paying, talk to your lender as soon as possible.

When to Consider a Peer-to-Peer Loan

You might wonder when a peer-to-peer loan could be a good choice for you. Let’s look at some situations.

If you have good credit, P2P loans can offer competitive interest rates. You might even find rates better than some banks. This can save you money over time.

Also, if you need funds quickly, a P2P loan could be a good option. The process can be faster than with traditional banks. Some platforms, like Prosper, offer quick funding. Upstart also sends funds quickly.

Furthermore, consider a P2P loan for debt consolidation. You can combine many debts into one loan. This can simplify your payments. Plus, you might get a lower interest rate. LendingClub even focuses on debt consolidation.

Finally, P2P loans can be helpful if you can’t qualify for traditional loans. Some platforms have more flexible requirements. For example, Upstart works with borrowers who have limited or no credit history. Kiva has no least credit score required.

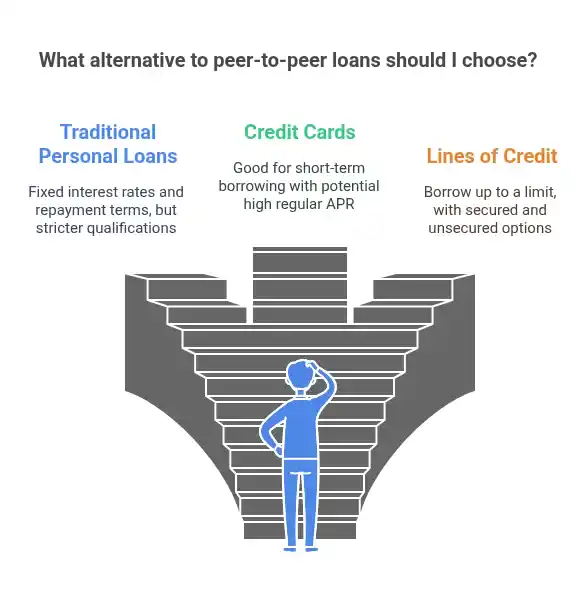

Alternatives to Peer-to-Peer Loans

Sometimes, a peer-to-peer loan might not be the best fit. Luckily, there are other options to consider!

One common alternative is traditional personal loans from banks or credit unions. These loans often have fixed interest rates and set repayment terms. However, they might have stricter qualification requirements.

Credit cards are another option, especially those with 0% intro APR. This can be good for short-term borrowing. But, be careful with the regular APR, as it can be high.

You can also look into lines of credit. These let you borrow money up to a lismit. There are secured options like HELOCs and unsecured personal lines of credit.

Borrowing from family or friends is another route. You might get better terms, but clear agreements are important to avoid issues.

Interestingly, LendingClub used to be a P2P lender but now funds loans directly. They can be a good option, especially for debt consolidation, as they can pay your creditors directly. They offer loan amounts from $1,000 to $40,000.

Investing in Peer-to-Peer Lending

So, you’re curious about investing in peer-to-peer lending? It can be an interesting way to grow your money!

To start, you’ll usually create an online account on a P2P platform. Then, you deposit some funds into your account. After that, you can buy notes, which are like small pieces of different loans.

Now, let’s talk about balancing risk and reward. You could see attractive returns, maybe between 5% and 9%. This can be higher than savings accounts. But, remember there are risks. Borrowers might not pay back their loans. Also, the platform itself could have problems. Your investment is usually not FDIC-insured.

It’s really important to diversify your investments. Don’t put all your money into just one loan. Instead, spread it across many different loans. This helps lower your risk if one borrower doesn’t pay.

As borrowers repay their loans, you’ll get some of the money back. You can choose to reinvest these payments. This can help you keep earning returns over time.

Platforms like Prosper often let you start investing with as little as $25. You might also be able to invest through traditional or retirement accounts. Some platforms even have automated investing options. These tools can help you choose and manage your investments based on your preferences.

The Future of P2P Lending and Distributed Cloud Technology

The future of P2P lending looks promising with new technologies like distributed cloud services. These services, such as Hivenet, can bring some cool advantages to P2P platforms.

One big benefit is enhanced data security. With decentralized storage, your information is spread out. This makes it much harder for bad guys to break in and steal data.

Another plus is lower infrastructure costs. Instead of relying on expensive data centers, P2P platforms can use distributed cloud power. This can save them a lot of money.

Improved uptime and scalability are also key. A distributed system means the platform is more reliable. It can also handle more users and activity without slowing down.

Using a distributed cloud can even have a reduced environmental impact. It uses existing resources, which is more eco-friendly than big, energy-hungry data centers.

For example, one P2P platform focused on small businesses used Hivenet. They saw their costs go down and their security get better. Plus, their platform could handle more activity easily.

Looking ahead, the future of P2P lending might involve more decentralization. Security and cost efficiency will also be really important. Distributed cloud technology can help make this happen.

Frequently Asked Questions (FAQs)

Let’s dive into some frequently asked questions about P2P lending!

What is the main difference between P2P lending and traditional bank loans?

The main difference between P2P lending and traditional bank loans is where the money comes from. In P2P lending, individuals lend to other individuals. Banks use money from their depositors to fund loans. Also, P2P isn’t always FDIC-insured.

Are peer-to-peer loans safe?

For borrowers, they should be as safe as traditional loans. Lenders take on more risk. Their money is usually not FDIC-insured. This means they might not get their money back if a borrower defaults.

What credit score do you need for a P2P loan?

This varies by platform. A higher score often means better terms. Some platforms, like Upstart and Kiva, may accept lower scores or no credit history. For example, Upstart’s minimum can be 300. Prosper might look for 640+. LendingClub may prefer 660+.

How does P2P lending affect my credit score?

Applying for a loan can cause a temporary dip due to a hard inquiry. But, making timely payments can help improve your score over time. It’s good to check if the lender reports to credit bureaus.

What are the risks involved in investing in peer-to-peer loans?

One big risk is borrower default. Platforms can also face instability. Remember, your investment is usually not FDIC-insured. To manage risk, diversify your investments.

Can I pay off my peer-to-peer loan early without penalties?

Often, yes. Many lenders, like Prosper and Upstart, don’t charge prepayment fees. LendingClub also has no prepayment penalty. Always check your loan agreement to be sure.

How quickly can I receive funds from a peer-to-peer loan?

This can vary, but it’s often faster than traditional loans. Some platforms offer approval quickly. You might get funds as soon as the next business day. However, it could take up to a week in some cases.

What are P2P lending platform fees?

Platforms can charge fees to borrowers, lenders, or both. Borrowers might see origination fees, late fees, or bounced payment fees. Lenders might also face certain fees. Always read the terms carefully to understand all costs.

How big is the P2P lending market?

It’s a growing market! In 2023, the global market was worth $5.94 billion. Projections say it could reach $30.54 billion by 2032.

How do you invest in P2P lending?

You usually create an account on a P2P platform. Then, you deposit money to fund loans. You can often select the types of borrowers you want to lend to based on their risk profiles. Some platforms even have automated investing options. You can also invest in some P2P companies by buying their stock.

Conclusion

So, let’s wrap up our discussion on peer-to-peer lending. It’s a really interesting way to borrow and invest money.

For borrowers, P2P lending can offer some great benefits. You might find it easier to apply. Sometimes you can even get better loan amounts. If your credit isn’t perfect, you might still qualify. Plus, interest rates can be lower than on credit cards.

However, remember that repayment terms might be shorter. Also, keep an eye out for potential fees. Always understand the terms before you borrow.

For investors, P2P lending can be a chance to earn more interest. You could see better returns than with regular savings. But it’s important to know about the risks. Your money isn’t insured like it is in a bank. There’s also a chance the borrower won’t pay back the loan.

So, if you’re thinking about P2P lending, do your homework! Research different platforms carefully. Compare what they offer for both borrowers and investors.

The world of P2P lending is always changing. New technologies might make it even better in the future. It’s a space worth watching if you’re looking for different ways to handle your finances.